- Details

- Written by Gordon Prentice

(Above: Darryl Gray (Chair) and Tracy Munusami (CEO) present the Library's "Report to the Community 2024" to Newmarket Councillors on 7 April 2025.)

Next Wednesday, at 5.30pm on 17 December 2025, I shall be addressing the Board of Newmarket Public Library on the conduct of its Chief Executive, Tracy Munusami. The meeting is open to the public but is not streamed. The text of my deputation which was emailed to the Library on Friday 5 December 2025 is set out below.

The Board Chair, Darryl Gray, told me on 2 December 2025:

"Tracy will be bringing a report to the upcoming Board meeting that aims to address your various concerns, and, I trust, bring some resolution to this matter."

The Board agenda is here.

DEPUTATION TO LIBRARY BOARD: 17 December 2025

The Conduct of the Chief Executive: Tracy Munusami

My deputation focusses on two concerns

- The definition now used by Newmarket Public Library for “active cardholders” which differs significantly from the Provincial definition and

- The quality and accuracy of the statistics which are presented to the Board and to the wider public. These are selective and are designed to mislead.

The Definition: The Board has an oversight role to ensure the Library operates within all applicable rules including guidance from the Province. It also has a fiduciary responsibility.

Last year, Newmarket Library received $74,494 from the Province and an operating grant from the Town of $3,781,775. Provincial grants only go to libraries which complete the Annual Survey of Public Libraries. They are expected to follow the guidance on how to complete the form.

The Chief Executive has been in post for over four years and on 7 April 2025 accurately told councillors:

“The definition of an “active library user” is someone who's used the library in the last 24 months… We do a survey every year to the Ministry. It's called the Annual Public Library Survey and that's the definition that they use.”

One week later she unilaterally changed the definition without approval of the Library Board or, so far as I can gather, the Board Chair.

The Board Chair told me as recently as 19 November 2025:

“I can confirm that we continue to report on active card holders using the provincial requirements and definition.”

This is incorrect.

The Chief Executive now defines an “active cardholder” as a NPL member with an unexpired library card regardless of whether it is used or not.

She substituted her own definition for the Provincial one knowing that it would boost membership numbers – the key metric widely used for assessing the success (or otherwise) of the library. On 4 July 2025 the Chief Executive told me:

We now define an active cardholder as someone who still has access to the library collection. If your card expires, you no longer have access to the library collection and are no longer an active cardholder until you return to renew it.”

I explained the consequences to the Board Chair in my email to him of 20 November 2025[1]:

Membership in both the Provincial and Newmarket definitions lasts for two years. The two years is not an issue. But Newmarket’s new definition removes the requirement to use the card within the two-year period.

We know from what the Chief Executive has told us that outreach sign-ups, for example, are not tracked to see if or when these new members first use their card to access library services. So, the library has no way of knowing when they become “active cardholders” according to the Provincial definition.

The Statistics Dashboard as presented to the Board uses the terminology “active memberships” and “new memberships”. Not active cardholders.

But when the Board receives the end of year total for “active memberships” the figure will need to be adjusted to meet the Provincial definition of active cardholder which involves using the card – not merely being in possession of one.

If it is not adjusted, the figure reported to the Province will be incorrect.

As I write this (Thursday 4 December 2025) the Board Chair has still not addressed this issue.

The Board should return to the status quo ante, reject the Chief Executive’s new definition and follow the provincial guidance.[2]

Misleading Statistics:

The Chief Executive presided over a data “modernisation” project which was part of the integration of the Library IT department and the Town’s.

Key data is now withheld from the Board but it is still available to the Chief Executive by using NPL’s specialist software (known as “Polaris: integrated library system”).

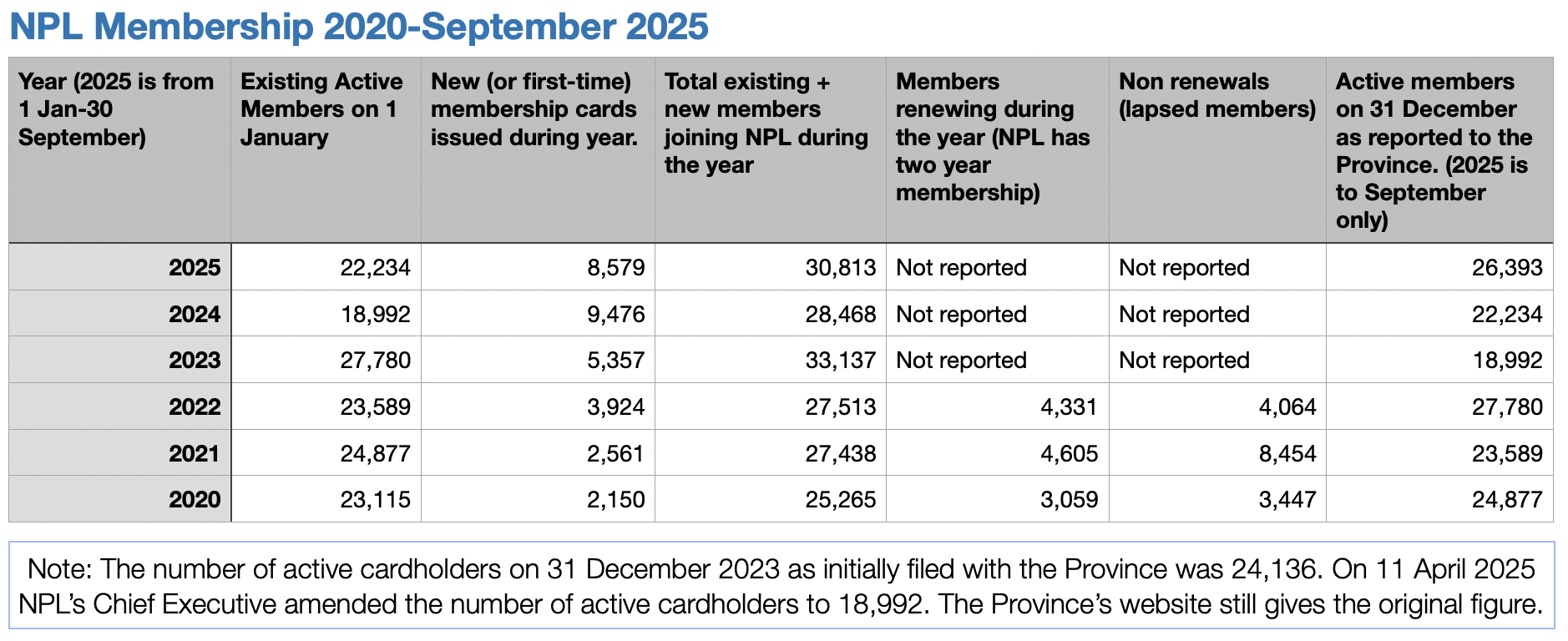

The Board receives data on new members and those new members signed up through outreach but not on members who have renewed or lapsed.[3] This deliberate decision to hold back key data makes it difficult if not impossible for the Library Board to make a proper assessment of the Library’s performance. The decision not to track members signed-up through outreach to see if they actually use the library is inexplicable given the emphasis the Board has placed on outreach work.[4]

The library has said this would infringe the privacy of members but the law of Ontario and the library’s own privacy policy allows for the collection of such information.[5]

Library membership has only three variables: new members, renewing members and lapsed members. The Board gets figures on the first and this exclusive focus on new members distorts the true picture.

In 2024 the Library issued 9,476 membership cards to “first-time” members. This represents 42.6% of all members, up from 28.2% in 2023. These figures are way above trend with figures in the low to mid-teens going back to 2014.

When I asked the library if I could see the Excel spreadsheet and the formulas to see how the figures were generated, my request was refused. I reluctantly appealed to the Information and Privacy Commissioner who is currently making enquiries.

In her quest for higher membership numbers the Chief Executive has deliberately misled the Board and its Chair.

Conclusion: What action am I requesting?

- The Library Board and the Chief Executive should follow the definition of “active cardholder” as set by the Province. And the figure reported to the Province in the Annual Survey of Public Libraries should be included in the Library’s “Report to the Community 2025”

- The Chief Executive should report to the Library Board quarterly on membership renewals and lapses. The Board may wish to consider asking the Chief Executive for an annual report on the split between Newmarket and out-of-town (or non-resident) members and Library membership by ward. The Board has received such reports in the past. The latter at the request of Councillor Bisanz.

- The Chief Executive should be asked to give a presentation to the Board on the capabilities of Polaris to aid members’ understanding of what it can do.

I would welcome questions.

Gordon Prentice

Member, Newmarket Library.

[1] See Appendix 1.

[2] See Appendix 2. Definitions

[3] See Appendix 3. Membership and Active Cardholders 2020-September 2025

[4] See Chronology 11 November and NPL’s Privacy Statement in Supplementary Materials

[5] See NPL Privacy Statement at Appendix 4.

Click "read more" below to see the chronology and supplementary material.

This email address is being protected from spambots. You need JavaScript enabled to view it.

Read more: The Conduct of Newmarket Public Library's Chief Executive, Tracy Munusami

- Details

- Written by Gordon Prentice

Easyhome, the nationwide franchise chain with a branch here in Newmarket, is making a pitch for a slice of the Christmas gift market.

“Make their Season Merry. Find the perfect gift from any store and pay at your own pace.”

Their flyer tells me I can get a HISENSE 50” QLED 4K UHD 60HZ- FIRE TV:

“Yours for only $9.99 per week”

You can get one of these Hisense TVs at Best Buy for $319.99 or from Walmart for $369.99.

Easyhome doesn’t tell you how much the “buy now” price is because, I suppose, they are not in that line of business. They lease so you can own… one day.

The cost of owning the same TV via the easyhome route is $1,558.

But you’ve got to work that out for yourself by combing through the fine print. The lease term for the Hisense TV is 156 weeks.

Of course, not everyone can afford to spend $320 on a Christmas gift. There are thousands of people here in well-off Newmarket who struggle to pay the bills. Easyhome's business model proves the point.

Fine print can be Painful

The small print at the bottom of the leaflet says:

“We know that fine print can be painful, but we believe it’s important for you to have all the facts!”

Easyhome is being economical with the truth. The APR is 29.9% but the painful fine print says:

“The Annual Percentage Rate “APR” of 29.9% is calculated from the cost of the product. The APR is from a representative lease and may not be the same for all advertised merchandise.”

Tantalisingly, the flyer says you can

“Get up to 12 months off your lease”.

But it’s not immediately obvious that doesn’t apply to the TV where the weekly payment is $9.99 and the "12 months off" offer only applies to weekly lease payments of $15.99 a week or more.

"The Term Reduction does not impact scheduled payment amounts, is calculated based on the original term of the new lease agreement and is applied at the end of your lease."

I’m not entirely sure what all that means.

Second Hand

But I do understand easyhome when they say:

“Advertised merchandise may not be exactly as shown. The photographs in this advertisement are representative and may been (sic) enlarged to show detail.”

And, astonishingly,

"Merchandise may be new or previously enjoyed.”

Not to put too fine a point on it, that means second hand.

And once you sign on the dotted line you are on the hook:

“Easyhome cannot accept returns for the product once it has been delivered to you.”

Financial Literacy

The easyhome flyer arrived a couple of days after one from our new Conservative MP, Sandra Cobena, former banker with the TD. She was reminding us that November is “Financial Literacy Month”. She was having a go at Carney and the Liberal Budget.

But, closer to home, what does she think about easyhome?

This email address is being protected from spambots. You need JavaScript enabled to view it.

Note: GoEasy is the holding company. LendCare (see Star article below) and easyhome are subsidiaries.

Update on 4 December 2025: From the Toronto Star: "Inside this Ontario loan company, concern grew as payments stopped. Its plan to keep bad debt off the books came at the expense of vulnerable borrowers."

Click "Read more" for the fine print

- Details

- Written by Gordon Prentice

Newmarket Public Library’s new definition of an “active member” will dramatically inflate the Library’s membership numbers.

Last year, in his foreword to the Library’s Report to the Community 2024, Board Chair Darryl Gray proudly announced:

“This past year has been extraordinary for the Newmarket Library, marked by significant growth in membership and an expanded presence throughout our community.”

Hold on to your hat because membership increases in 2025 could be truly spectacular.

The Library has changed its definition of an “active cardholder” from someone who uses their library card at least once in a two-year period (the Provincial definition) to someone who has an unexpired library card - whether they use it or not.

It is not clear when - or if - the Board approved this change which, on the face of it, doesn’t square with the Provincial definition. (Photo right: Library Board Chair, Darryl Gray, and Library Chief Executive Tracy Munusami at the 17 September 2025 Board meeting.)

The latest active cardholder figures will be considered by the Library Board on Wednesday (19 November 2025).

These show 26,393 active members at the end of September with three months still to run in 2025. If this trend continues for the rest of the year, this puts active membership on course for a 11 year high - or since on-line records have been posted. It could be the best ever.

Outreach

Since the appointment of the current Chief Executive, Tracy Munusami, in August 2021 membership growth has become the defining statistic used to measure the Library’s success.

Recruiting new Library members through outreach is a crucial component of the new strategy.

People are signed up in bulk, for example, in schools.

But, because a card is issued, it does not follow that it will be used.

Astonishingly, the Library chooses not to track members recruited through outreach to see if they actually use their card to access library services and are not just sleeping members.

The Chief Executive says collecting this information would infringe the privacy of library members but that’s a bogus argument. No personal details would be sought or required – just the aggregate statistics.

The latest figures to be presented to the Library Board on 19 November 2025 show that in the July-September quarter of this year, over 23% of new members came through outreach.

Annual Survey of Public Libraries

To be eligible for Provincial library grants, all Ontario libraries are required to submit data to the Province annually for inclusion in its Annual Survey of Public Libraries (ASPL). Last year, Newmarket Library received $74,494 from the Province. (The Town’s operating grant to NPL was $3,781,775.)

The Province requires libraries to count “active cardholders” who are defined as:

“library cardholders who have used their library card in the past two years.”

As I say, Newmarket Public Library now defines an “active cardholder” as someone who holds an unexpired membership card. The Chief Executive says this “aligns” with the Provincial definition.

Plainly, it doesn’t.

Ms Munusami insists:

“A library card provides access to a wide range of resources: digital and physical materials, programs, spaces, and services. We do not monitor or track individual usage, and there are no systems in place to measure all the possible ways one can access the many types of library services (i.e., main branch, vending machines, alternative locations, programming, or online services).”

These arguments are specious. The Library currently tracks the use of on-line services and the lending of books and digital materials which are accessed by a library card to get the usage totals which are shown in the Statistics Dashboard.

Members of the public who are not library members can use its public spaces, consult books and other reading materials, book rooms and use the computers. The Library does not - and never has – tracked any individual’s use of the Library. The video here shows what NPL's integrated library system Polaris can do.

It can effortlessly pull up the names of patrons to see when, for example, they last used their library card.

But the Library doesn't spy on members to see what they are borrowing.

The segment above is part of an Odin Workday tutorial on creating and using record sets.

Contradiction

When I flagged up the clear contradiction between Newmarket’s new definition and the Provincial one, I was told by Deborah Cope, a civil servant at the Ministry of Tourism, Culture and Gaming:

"The definitions are intended as guidelines to assist libraries in filling out the surveys as best they can, while understanding each library may have different systems in place to capture active users. (My underlining for emphasis).

We do not have concerns with the data that the Newmarket public library has shared to date. We will continue to work with all public libraries, including Newmarket Public Library, to support them as they fill out the survey each year."

If the Province wants data from libraries across Ontario which reflects its own definition of active users it needs to offer advice and guidance to Newmarket Public Library before Ms Munusami files her survey for 2025.

Otherwise, across the Province, it's garbage in and garbage out.

Membership renewals

The Library has also stopped publishing data on membership renewals – a key statistic when assessing membership retention.

At the Board meeting on 17 September 2025 Library Vice Chair, Councillor Kelly Broome, asked the Library Chief Executive about the reported 9,476 new or first-time members who joined the Library in 2024:

“And those are new memberships for the year 2024?”

Tracy Munusami nods yes.

Kelly Broome:

“Renewed memberships?”

Tracy Munusami:

“New memberships.”

Board members and the public no longer get statistics on renewed and lapsed membership. But the figures are available within the library.

What Needs to be Done

The selective use of statistics can be misleading.

The Statistics Dashboard, which was only recently introduced as a regular agenda item, goes to the Board on a quarterly basis. The range of data should be expanded to include:

- Membership renewal figures. (And the membership renewal figures for 2024 should also be published.)

- Lapsed membership.

- New Memberships signed up through outreach showing how many new members have actually used their membership card after, say, one year to access Library services.

This email address is being protected from spambots. You need JavaScript enabled to view it.

- Details

- Written by Gordon Prentice

Former MP, Tony Van Bynen, has plans to replace Matt Gunning as Chair of the Newmarket-Aurora Federal Liberal Association with his own favoured candidate at its AGM tomorrow, Sunday 19 October 2025.

He stood down at the last election saying (yet again) he was retiring to spend more time with his family.

Newmarket-Aurora was one of 19 ridings across the country lost by the Liberals in the Federal election in April.

Their candidate, Jennifer McLachlan, replaced the bland old banker Tony Van Bynen who joined the Liberal Party in his late sixties with the sole intention of becoming the area’s MP. He was the only person to throw his hat into the ring and to my general amazement ended up in the House of Commons where he quietly followed the Party line and read his occasional speeches word-for-word in a monotone from a leather binder.

By temperament he is timid and cautious, never showing his hand until he has, in his own words, “scoped things out”.

When he came out publicly against Trudeau I knew the then Prime Minister’s days were numbered.

Surprise

So it comes as a bit of a surprise to learn Van Bynen has been manoeuvring to replace the Chair of the Newmarket-Aurora Federal Liberal Association, Matt Gunning, at tomorrow’s AGM.

My spies tell me Van Bynen’s hand-picked candidate for Chair is Laura Bradford who was Jennifer McLachlan’s Deputy Campaign Manager. Van Bynen will run as her deputy.

I am told Van Bynen was the driving force behind Jennifer McLachlan’s acclamation and vouched for her.

During this year’s Federal Election campaign I winced every time I heard McLachlan gush about Van Bynen as if the old banker walked on water.

“I am new to politics and I have some learning to do. I have Mr Van Bynen who has been mentoring me over the last while and he will continue to support me while I head to Ottawa and work with the community after. People always ask how are you gonna fill his shoes? And I say there's no chance I will fill his shoes but he's passed me the torch. So let's see how fast I can go with it and run around this riding as much as I can.”

Oh dear!

Jennifer’s mentor should have told her you never take the voters for granted. Never even hint the election is in the bag. And she compounded the error by saying Van Bynen would take her under his wing and offer support while she “heads to Ottawa”.

No Platform

So far as I can gather, neither Bradford nor Van Bynen is running on a platform so local liberals have no idea what they are promising other than a change of faces at the top table.

This kind of challenge is, apparently, unusual. Matt Gunning has been Chair of the Association for seven years or more and his Deputy, Shameela Holden-Shakeel, for the past two years.

I don’t have any problems with annual elections and people challenging incumbents. Not at all.

But Van Bynen and Bradford should at least tell local Liberals why they are running.

Sandra Cobena and the Deficit

Meanwhile, in another part of the forest, Sandra Cobena, our new Conservative MP (and yet another banker) has been settling in, without the need of any mentoring.

She is on the Standing Committee on Finance and takes every opportunity to denounce the Liberal’s record on the National Debt and deficit.

On 9 October 2025 she was at it again, making yet another theatrical plea for a balanced budget:

“I truly wish that the government would be honest and would focus on balancing the budget and reining in spending so that we can actually have a future for our children. We cannot spend our way to affordability. We cannot continue to spend and spend and pretend there are no consequences”

Too bad she is silent when it comes to Doug Ford’s Ontario where we are promised a balanced budget in 2027 - but don't hold your breath.

Ford became Premier way back in 2018 and brazenly bought popularity with bribes and give-aways. It worked. Balancing the budget - totemic for most Conservatives - has never been much of a priority for Ford. Popularity comes first.

Our Progressive Conservative MPP, Dawn Gallagher Murphy, ignores the red ink and trills that Ontario is “maintaining a path to a balanced budget”.

Ontario's Finances in Poor Health

This fancy dancing hasn't gone down well with the right wing free-market think tank, the Fraser Institute, which says Ontario’s finances are in poor health.

I wonder what Sandra Cobena thinks about this.

Pity she’s not saying.

This email address is being protected from spambots. You need JavaScript enabled to view it.

NAFLA will be holding its AGM at 2pm on Sunday 19 Oct at the New York Region Foodbank at 17665 Leslie St Unit 19, Newmarket, ON L3Y 3E3.

Update on 20 October 2025: Matt Gunning and Shameela Holden-Shakeel were voted out at yesterday's AGM. The new Chair and Vice Chair are Laura Bradford and Tony Van Bynen.

The Federal Budget is on 4 November 2025

Click "read more" for Sandra Cobena on the National Debt

Read more: Tony Van Bynen plots regime change at tomorrow's Liberal Association AGM

- Details

- Written by Gordon Prentice

Progressive Conservative MPP, Dawn Gallagher Murphy, celebrated her 4th Annual Taxpayer-funded BBQ yesterday at Riverwalk Commons in downtown Newmarket.

It was a beautiful warm and sunny Sunday afternoon and there was a decent sized crowd queuing up for their "free" meal.

Of course, there’s no such thing as a free lunch and those registering beforehand and those registering on the day will probably have their names harvested for Dawn’s database. Just to remind them of the dates of her future BBQs - and her legendary largesse when it comes to spending other people's money.

No Famous Faces

I was there for about 45 minutes – without a hamburger or spring roll passing my lips – and I didn’t see too many familiar faces.

No sign of the Mayor or any councillors but they could have been late arrivals.

I chatted to the on-duty paramedics about the Government’s plans to ban municipal speed cameras and wondered how that would impact their work. Likewise, I talked to the firefighters asking for their views - all off-the-record.

Enthusiastic

The irrepressible former Council candidate, Darryl Wolk, was there as always, enthusiastically waving the flag for the Progressive Conservatives, right or wrong. (Photo below)

Darryl is an amateur wrestler in his spare time and explains the tricks of the trade, the feints, the phoney slams and the smacks. It’s all about the spectacle and entertainment. A bit like Dawn's politics.

Darryl stresses you never hurt your opponent – at least, not intentionally.

Expenses

We shall find out in due course how much Dawn Gallagher Murphy's latest BBQ cost us when she files her "hospitality" expenses. This email address is being protected from spambots. You need JavaScript enabled to view it.

But I got the impression she has scaled things back a bit with the Provincial election now safely behind her.

During her first term as Newmarket-Aurora MPP she spent an eye watering $26,995 of taxpayers’ money on her BBQs.

Centre of attention

She laps up her minor-celebrity status. Loves being the centre of attention.

During the entire time I was there, she was busily at work, playing the part, being photographed on the stage with a long line of admirers.

I doubt if anyone asked her why she wants to ban municipal speed cameras across the Province.

On such a jolly day it would have struck the wrong note.

After all, it's not really something to laugh about.

This email address is being protected from spambots. You need JavaScript enabled to view it.This email address is being protected from spambots. You need JavaScript enabled to view it.

Page 3 of 288